Single-vehicle accidents trigger carrier surcharges through collision claims even without a citation—and the rate impact varies wildly based on whether you file through collision coverage or pay out-of-pocket.

How Carriers Price Single-Vehicle At-Fault Accidents

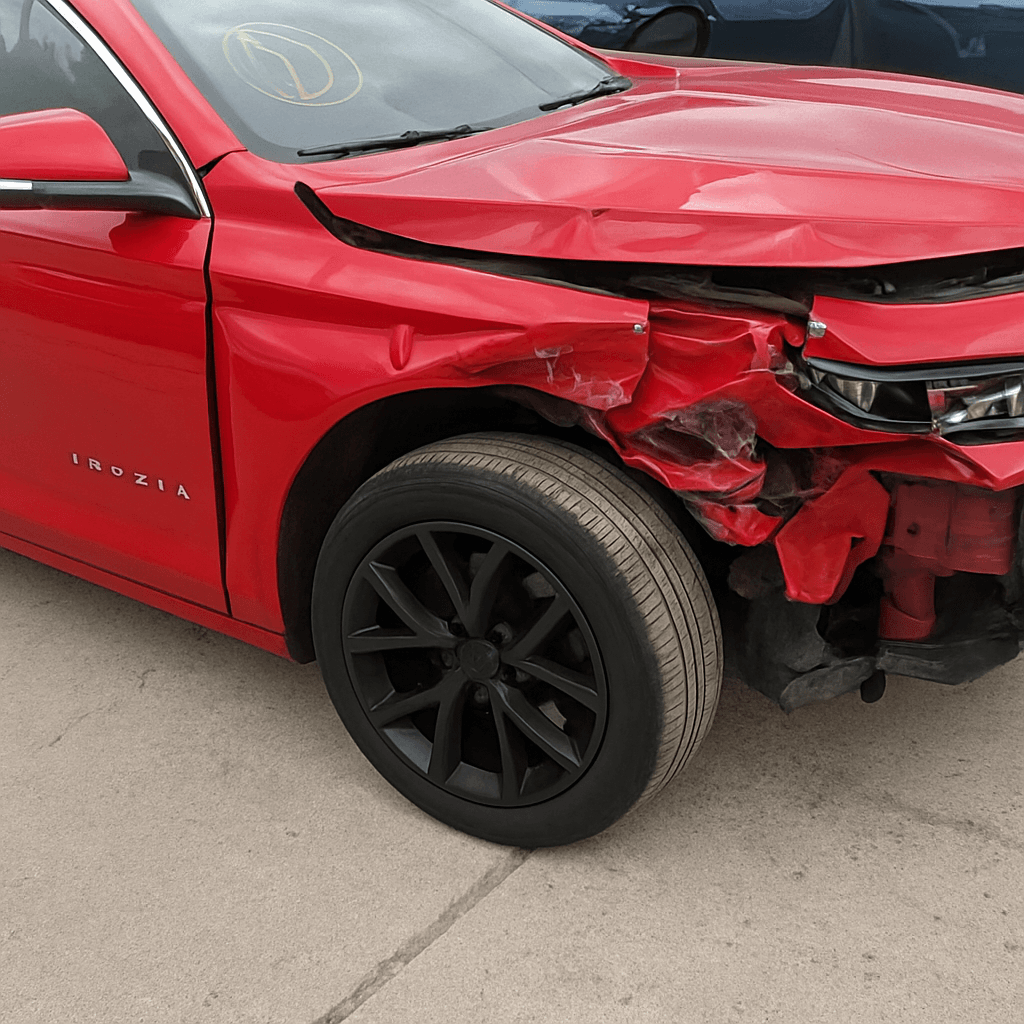

You hit a guardrail, slid into a ditch, or clipped a pole backing out. No other driver involved. No citation issued. Most drivers assume this stays off their insurance record if they pay for repairs themselves—but that assumption breaks down the moment you file a collision claim.

Carriers classify single-vehicle at-fault accidents as chargeable claims the instant you file through your collision coverage, regardless of whether law enforcement responded or a ticket was issued. The claim enters your record through the Comprehensive Loss Underwriting Exchange (CLUE), a national database that tracks insurance claims for seven years. Every carrier you quote with for the next three to five years will see it.

Surcharge structure varies dramatically by carrier. Some classify single-vehicle incidents as minor claims, applying 15-25% rate increases for three years. Others group them with major at-fault accidents, triggering 40-60% surcharges lasting five years. The difference isn't based on damage severity or fault clarity—it's internal tier classification rules carriers don't disclose until your renewal notice arrives. A $3,000 guardrail repair at one carrier might cost you $1,200 over three years in premium increases, while the same claim at another carrier costs $4,800 over five years.

The Break-Even Calculation Most Drivers Skip

Filing a collision claim makes financial sense only when repair costs exceed your deductible plus the total premium increase over the surcharge period. That's not the math most drivers run. They compare repair estimate to deductible, file the claim, and discover the real cost at renewal.

Here's the actual formula: Add your deductible to the estimated surcharge. If your current premium is $140/month and your carrier applies a 25% surcharge for three years after a minor claim, that's an additional $35/month for 36 months—$1,260 total. Add your $500 deductible and the true claim cost is $1,760. If repairs cost $1,600, you lose money by filing.

The calculation shifts if you're already in a high-risk tier. Drivers with prior violations or claims face steeper surcharges because carriers stack penalties—a second chargeable event within three years often doubles the rate impact of the first. If you're quoted SR-22 coverage or classified as non-standard, a single-vehicle claim can push you into assigned risk pools where premiums jump 70-120%. At that tier, paying $4,000 in repairs out-of-pocket often beats filing a $5,000 claim.

Find out exactly how long SR-22 is required in your state

When Single-Vehicle Accidents Trigger Violations Anyway

No other party doesn't always mean no citation. Officers responding to single-vehicle accidents frequently issue tickets for unsafe speed, failure to control, or reckless driving based on scene evidence—skid marks, damage patterns, road conditions. Those violations carry separate surcharges that stack on top of any collision claim penalty.

Some states mandate reporting for single-vehicle accidents above specific damage thresholds. If repair costs exceed $1,000 to $2,500 depending on state, you're required to file an accident report with the DMV even if you don't file an insurance claim. That report creates a state record that carriers access during underwriting. You avoid the claim surcharge by paying out-of-pocket, but the accident itself still appears on your driving record and may trigger a rate adjustment.

Carriers also access police reports independently through vendor partnerships. If an officer filed a report—even without issuing a citation—your insurer may learn about the incident at renewal and reclassify your risk tier based on the accident description. The surcharge appears as an "underwriting adjustment" rather than a claim penalty, but the financial result is identical.

How Claim Timing Affects Your Rate Window

Carriers apply surcharges at the first renewal following claim closure, not the accident date. If your policy renews monthly, the increase hits 30-60 days after your claim settles. If you're on a six-month term, you might drive four months before seeing the impact.

That delay creates a decision window most drivers waste. Once you file the claim, it enters CLUE immediately—you can't un-file it. But you can shop carriers before your current insurer applies the surcharge. Some carriers tier single-vehicle accidents more favorably than others, and switching before renewal lets you lock in a lower base rate that the surcharge then applies to.

The surcharge clock starts from claim closure date and runs for a carrier-specific period—typically three to five years. After that window closes, the claim remains on your CLUE report for up to seven years but stops affecting your rate at most carriers. Shopping again at the three-year mark often produces significant savings as you exit the surchargeable period at your current insurer while other carriers may still penalize the older claim.

Why Accident Forgiveness Doesn't Always Apply

Accident forgiveness programs waive the surcharge for your first at-fault claim, but most carriers exclude single-vehicle accidents from eligibility or apply restrictions that void coverage after the fact. The exclusion appears in program fine print, not marketing materials.

Common restrictions: forgiveness applies only to accidents involving another vehicle, or only to claims below a specific dollar threshold, or only after you've maintained continuous coverage for three to five years without any claims. A guardrail hit two years into your policy might not qualify even though you purchased forgiveness at inception.

Some carriers revoke accident forgiveness retroactively if you file a second claim within the forgiveness period. Your first accident gets forgiven at renewal, your rate stays flat, then you file a second claim 18 months later. At the next renewal, the carrier applies surcharges for both claims retroactively, recalculating premiums back to the first accident date. You owe the difference as a lump sum or see a massive increase that reflects two surchargeable events.

What Post-Accident Carrier Shopping Actually Costs

Switching carriers after a single-vehicle accident triggers re-underwriting with the claim visible on CLUE. Some carriers specialize in post-accident coverage and apply lower surcharges than standard market leaders. Others won't quote you at all until three years post-claim.

Non-standard carriers and high-risk insurers often provide the most competitive rates immediately after a claim because they price all applicants in elevated risk tiers—your single-vehicle accident doesn't move you into a penalty bucket because you're already there. Standard carriers treat the same claim as a risk elevation event, applying steeper surcharges to move you from preferred to standard tier pricing.

Shopping costs time but rarely money if you're strategic. Request quotes 30-45 days before your renewal date, disclose the claim upfront, and compare total six-month or annual premiums rather than monthly rates. Carriers adjust payment plans and down payment requirements after claims—a lower monthly quote might require a 40% down payment instead of the standard 20%, raising your upfront cost even as the monthly figure drops.